Choosing between Pag-IBIG MP2 and regular Pag-IBIG savings (often called MP1 or Pag-IBIG I) is a common decision many Filipinos face. Both programs are managed by Pag-IBIG Fund, but their purposes, rules, and benefits differ significantly.

This article compares MP2 and regular Pag-IBIG savings across key dimensions so you can decide which option caters best to your financial goals.

This comparison is practical and research-backed. It references official Pag-IBIG rules, current dividend behavior, and real use cases so you can choose with confidence.

Quick Summary: MP2 vs Regular Pag-IBIG at a Glance

-

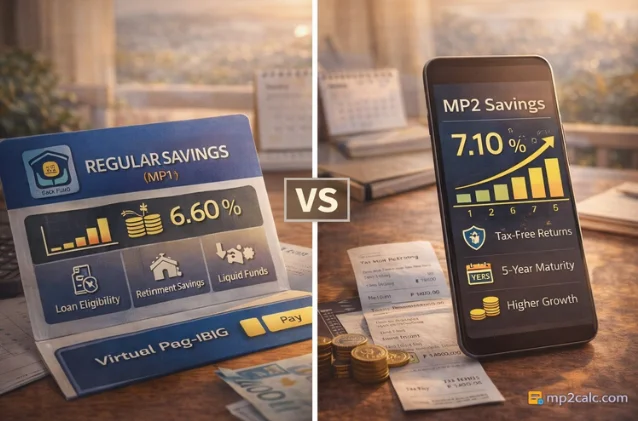

Purpose: Regular Pag-IBIG savings (MP1) are mandatory for many and tied to housing loan eligibility; MP2 is a voluntary savings program for higher returns.

-

Minimum contribution: MP1 monthly savings are based on mandatory contributions; MP2 minimum is ₱500 per remittance.

-

Maturity: MP1 savings are linked to membership and loans; MP2 has a fixed 5-year maturity.

-

Dividends: MP2 generally offers higher dividend rates than MP1 and dividends are tax-free for both.

-

Liquidity: MP1 funds are more liquid and can be used for loans; MP2 is less liquid until maturity.

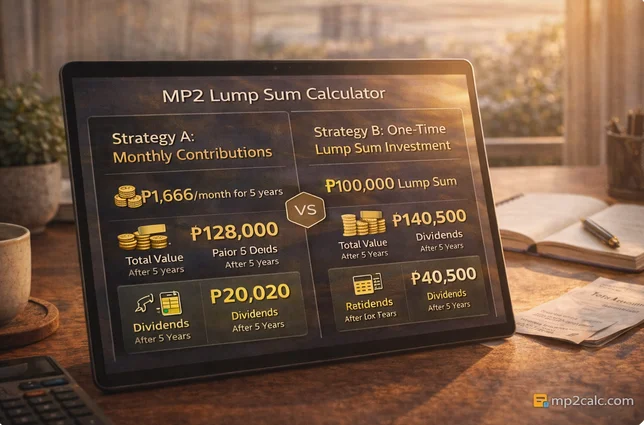

For detailed calculators, use our tools:

What Is Regular Pag-IBIG Savings (MP1)?

Regular Pag-IBIG savings—sometimes referred to casually as MP1—represent the standard contributions many workers make to the Pag-IBIG Fund. These contributions often involve employer and employee shares, and they serve multiple purposes:

-

Building mandatory savings for housing loans and various benefits

-

Qualifying members for Pag-IBIG loan programs

-

Providing a base balance that accumulates dividends over time

Regular Pag-IBIG savings are part of the social benefits system and are generally considered more liquid and geared toward loan-related use.

What Is Pag-IBIG MP2?

MP2, or the Modified Pag-IBIG II Savings Program, is a voluntary savings program introduced for members seeking higher returns on their savings. MP2 lets you choose how much and how often you want to save, with a low minimum of ₱500 per contribution.

Key MP2 features include:

-

Voluntary participation

-

Minimum ₱500 per remittance

-

Fixed five-year term (maturity)

-

Higher, dividend-based returns

-

Tax-free dividends

MP2 is best suited for medium-term savings goals where you can lock funds for five years and aim for higher returns than regular savings.

Head-to-Head Comparison: Key Factors

1. Purpose and Use

-

MP1 (Regular): Primarily serves as a membership savings and is tied to loan eligibility. It’s useful if you plan to apply for Pag-IBIG housing loans, calamity loans, or multi-purpose loans.

-

MP2: Purely a savings and investment vehicle for higher returns. It is not required for loan eligibility and is focused on growing assets.

2. Contribution Flexibility

-

MP1: Contributions are often regular and may include employer shares.

-

MP2: Contributions are flexible—monthly, annual, or one-time—based on what you can afford.

3. Minimums and Limits

-

MP1: Contribution amounts are usually defined by membership rules and payroll setup.

-

MP2: Minimum of ₱500 per remittance and no defined maximum.

4. Dividend Rates & Returns

-

MP1: Generally earns lower dividend rates compared to MP2.

-

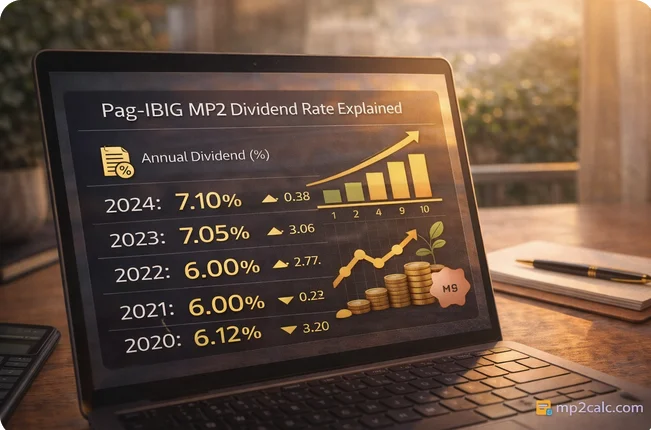

MP2: Historically offers higher dividends; uses fund performance to determine yearly rates.

5. Liquidity & Access

-

MP1: More liquid. Linked to loan programs; members can use accumulated savings as collateral or withdraw under specific conditions.

-

MP2: Locked-in for five years. Early withdrawal is allowed only under limited conditions like disability or retirement.

6. Tax Treatment

-

Both MP1 and MP2: Dividends are tax-free, which improves net returns compared to taxable bank interest.

Which Is Better for Different Goals?

If you want home financing or frequent loans

Choose regular Pag-IBIG savings (MP1) because it is tied to loan eligibility and employer-based contributions.

If you want higher returns and can lock funds for 5 years

Choose MP2 for potentially higher dividends and tax-free growth.

If you need short-term liquidity or emergency funds

MP1 or a separate emergency savings account is more suitable due to MP2’s 5-year lock-in.

Practical Examples (Use Cases)

Young professional saving for a down payment: Keep MP1 for loan eligibility and use MP2 for a medium-term growth vehicle if you can lock money for five years.

OFW with lump-sum remittance: MP2 lump-sum contributions often make sense because they maximize compounding over the five-year term.

Retiree looking for steady, low-risk income: MP2 can be part of a conservative portfolio for tax-free dividend income, provided liquidity needs are met.

How to Use Both Together (A Balanced Approach)

You don’t have to choose only one. Many members use a blended strategy:

-

Maintain mandatory MP1 contributions for employment and loan eligibility.

-

Open an MP2 account for extra savings and better returns.

-

Use calculators to plan contributions

This dual strategy combines liquidity, loan access, and higher long-term returns.

Things to Watch Out For

-

Dividend variability: MP2 returns depend on fund performance and may vary yearly.

-

Liquidity constraints: MP2 funds are less accessible until maturity.

-

Processing delays: Some users report delays in reflecting contributions or occasional misapplied payments; keep transaction proof when paying. (If in doubt, check your Virtual Pag-IBIG account.)

For claims and withdrawal processes, see the official Pag-IBIG claim page

Frequently Asked Questions (MP2 vs MP1)

1. Can I transfer funds between MP1 and MP2

No. MP1 and MP2 are distinct accounts and funds are not transferrable between the two.

2. Are MP2 dividends always higher than MP1

Not always, but MP2 is designed to offer higher dividends based on the fund’s investment strategy and profit allocation.

3. Can employer contributions go into MP2

Employer contributions typically go to regular Pag-IBIG savings. MP2 contributions are usually made by the member voluntarily.

Final Words:

For most savers, a combined approach is the most practical: keep your regular Pag-IBIG savings for loan access and mandatory benefits, and use MP2 for additional, medium-term savings where higher, tax-free returns are desired.

Note: This article reflects standard MP2 and Pag-IBIG practices. For official rules, dividend declarations, and claims procedures, consult Pag-IBIG Fund resources and your Virtual Pag-IBIG account.