One of the most common questions about the Pag-IBIG MP2 Savings Program is about its interest rate. Many people search for the MP2 interest rate expecting a fixed percentage similar to bank savings or time deposits.

In reality, MP2 does not use a traditional interest system. Instead, it earns through annual dividends, which is an important distinction every investor should understand.

Is There an MP2 Interest Rate?

Strictly speaking, Pag-IBIG MP2 does not have a fixed interest rate. What many people refer to as the MP2 interest rate is actually the MP2 dividend rate declared annually by Pag-IBIG Fund.

Unlike banks that pay guaranteed interest, Pag-IBIG distributes earnings to MP2 members in the form of dividends. These dividends depend on the fund’s overall financial performance for the year.

Because of this structure, MP2 returns can change annually, sometimes going up and sometimes going down. Understanding this difference is essential when comparing MP2 to other savings or investment products.

How Pag-IBIG MP2 Dividends Are Determined

Pag-IBIG Fund invests MP2 contributions in housing loans, government securities, and other approved investments. At the end of each year, the fund reviews its performance and declares a dividend rate for MP2.

Once declared, the dividend rate is applied to the average balance of each member’s MP2 account. The resulting dividend amount is then credited to the account and usually reinvested automatically, allowing it to earn dividends in future years.

This system means your MP2 earnings are closely tied to both your account balance and the annual dividend rate.

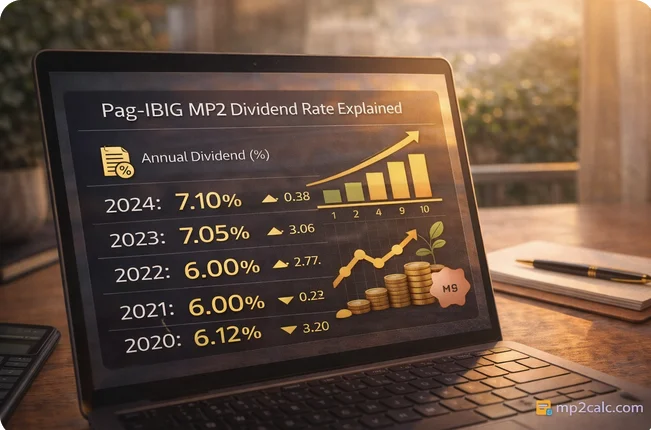

Historical MP2 Dividend Rates

Over the years, Pag-IBIG MP2 has delivered competitive dividend rates compared to traditional savings accounts. While rates are not guaranteed, they have often been attractive for conservative investors.

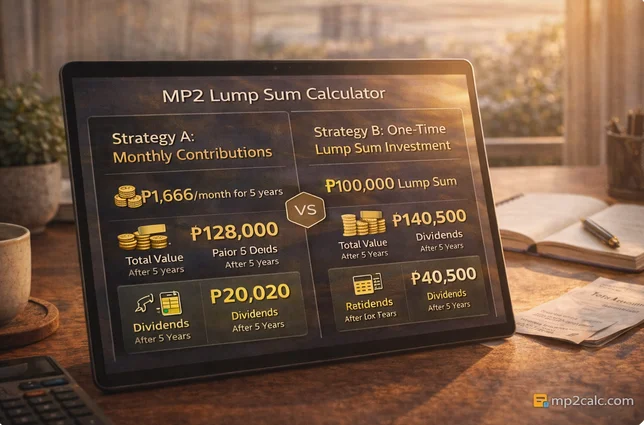

Dividend rates vary by year, which is why long-term planning should consider multiple scenarios rather than relying on a single percentage. To explore exact figures by year, you may refer to the MP2 Dividend Calculator or the upcoming MP2 Dividend Rate by Year guide.

For projections using the latest available rate, the Pag-IBIG MP2 Calculator provides an easy way to estimate potential returns.

How MP2 Dividends Are Calculated

MP2 dividends are calculated annually based on your account balance. Contributions made earlier in the year generally earn dividends longer than those made later.

Dividends are not compounded monthly or daily. Instead, they are credited once per year after the dividend rate is officially announced. Once credited, these dividends form part of your MP2 balance and earn dividends in subsequent years.

To see how this affects your earnings in detail, you may use the MP2 Dividend Calculator, which focuses specifically on dividend growth.

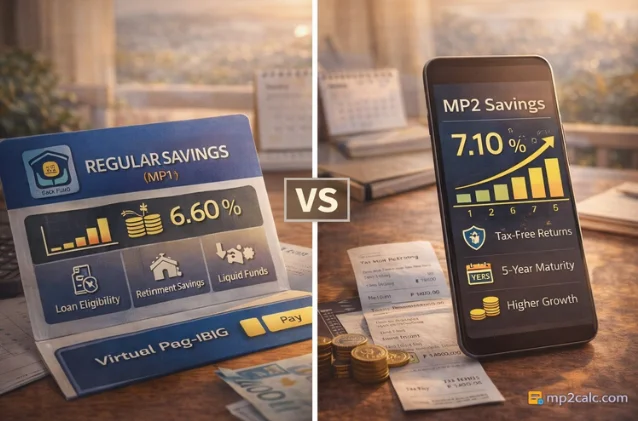

MP2 Interest Rate vs Bank Interest Rate

Comparing MP2 to bank savings requires understanding key differences.

Bank savings accounts offer fixed but usually lower interest rates and allow easy withdrawals. MP2, on the other hand, offers potentially higher returns but requires a five-year commitment.

MP2 dividends are also tax-free, while bank interest earnings are typically subject to withholding tax. This tax advantage often makes MP2 more attractive for long-term savers, even when headline rates appear similar.

How the MP2 Interest Rate Affects Your Final Savings

The dividend rate plays a significant role in determining how much your MP2 savings grow. Even small changes in the annual rate can lead to noticeable differences over five years.

However, the dividend rate is only one factor. Contribution amount, contribution timing, and consistency all influence your final savings.

To understand the combined effect of these factors, you can use the MP2 Maturity Calculator, which shows your estimated payout at the end of the five-year term.

Can You Choose or Lock an MP2 Interest Rate?

No. MP2 members cannot lock in a specific interest or dividend rate. Rates are determined annually and apply to all MP2 accounts for that year.

This is why MP2 should be viewed as a long-term savings program rather than a short-term yield product. The focus should be on consistent saving and long-term growth rather than chasing yearly rates.

Common Misunderstandings About MP2 Interest

A common misconception is that MP2 guarantees high returns every year. While MP2 has performed well historically, dividends depend on fund performance and economic conditions.

Another misunderstanding is assuming MP2 uses monthly compounding like some investments. In reality, dividends are credited annually, which affects how growth accumulates.

Understanding these points helps set realistic expectations and prevents disappointment.

Frequently Asked Questions About MP2 Interest Rate

Is the MP2 interest rate guaranteed?

No. MP2 uses dividends, not guaranteed interest, and rates depend on annual fund performance.

Why does the MP2 interest rate change every year?

Because dividend rates are based on Pag-IBIG Fund’s yearly earnings, they vary depending on economic and investment conditions.

Does MP2 compound interest monthly?

No. Dividends are credited once per year, then reinvested.

Final Thoughts

Understanding the MP2 interest rate means understanding how dividends work. MP2 is not about fixed returns but about disciplined saving backed by a government-managed fund.

When used correctly, MP2 can be a powerful long-term savings tool. To explore how dividend rates may affect your savings in practice, use the Pag-IBIG MP2 Calculator and related MP2 tools available on this site.