Many Pag-IBIG members rely on online calculators to estimate their MP2 savings, but understanding how Pag-IBIG MP2 is calculated manually gives you deeper confidence in your numbers.

When you know the formula and logic behind MP2 dividends, you can verify results, plan contributions more accurately, and avoid unrealistic expectations.

Why Learn to Calculate MP2 Manually

Manual calculation helps you understand how MP2 actually grows. MP2 does not follow the same rules as bank savings or fixed-interest investments. Dividends are credited annually, rates change yearly, and contribution timing matters.

By learning the manual method, you can:

-

Validate online calculator results

-

Understand why early contributions earn more

-

Compare different contribution strategies logically

-

Avoid confusion about interest versus dividends

Once you understand the process, tools like the Pag-IBIG MP2 Calculator become even more useful.

Key Concepts You Must Understand First

Before computing MP2 savings manually, it is important to understand three basic concepts.

First, MP2 uses dividends, not fixed interest. The dividend rate is declared once per year and may change annually.

Second, dividends are credited once per year, not monthly or daily.

Third, dividends are usually reinvested automatically, meaning they also earn dividends in later years.

These three rules shape every MP2 calculation.

The Basic MP2 Dividend Formula

The simplified formula for calculating MP2 dividends for a given year is:

Annual Dividend = Average Balance × Dividend Rate

Where:

-

Average Balance is the amount of money in your MP2 account during the year

-

Dividend Rate is the percentage declared by Pag-IBIG for that year

Once dividends are credited, the formula for the next year uses the new total balance, including previous dividends.

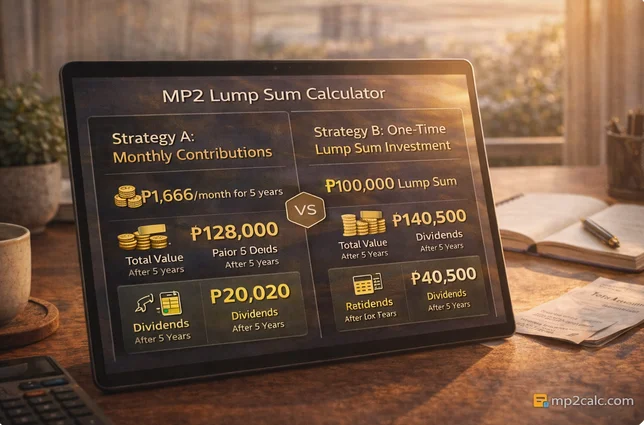

Example 1: One-Time MP2 Contribution

Assume you invest a one-time amount of ₱100,000 at the start of your MP2 term, and the declared dividend rate for the year is 7%.

The dividend for the first year would be:

₱100,000 × 7% = ₱7,000

Your new balance at the end of the year becomes:

₱107,000

In the second year, dividends are calculated based on ₱107,000, not the original ₱100,000. This demonstrates how reinvestment increases future earnings.

To automate this process over five years, you may use the MP2 Lump Sum Calculator.

Example 2: Monthly MP2 Contributions

Monthly contributions require more steps because deposits are spread throughout the year.

Assume you contribute ₱2,000 every month for one year. The total contribution for the year is ₱24,000. However, not all contributions earn dividends for the same length of time.

Early monthly deposits earn dividends longer than later ones. Pag-IBIG considers the average balance across the year when calculating dividends.

This is why monthly MP2 calculations are more complex to do manually. To simplify planning, you can use the MP2 Monthly Contribution Calculator.

Example 3: Five-Year MP2 Manual Projection

To calculate MP2 manually over five years, you repeat the same steps each year:

-

Determine your total balance for the year

-

Apply the declared dividend rate

-

Add the dividend to your balance

-

Repeat for the next year using the new balance

Because dividend rates may change annually, exact manual projections require assumptions for each year. This is why projections are estimates, not guarantees.

To see your expected payout after five years, you may refer to the MP2 Maturity Calculator.

Why MP2 Is Not Calculated Like Bank Interest

Bank savings accounts usually compute interest daily or monthly at a fixed rate. MP2 does not work this way.

MP2 dividends are calculated annually and depend on fund performance. This difference explains why MP2 returns can fluctuate and why comparing MP2 directly to bank interest rates can be misleading.

For a deeper explanation, see MP2 Interest Rate Explained.

Common Mistakes When Calculating MP2 Manually

One common mistake is assuming monthly compounding. MP2 does not compound monthly.

Another mistake is using a single dividend rate for all five years without considering changes.

Some people also forget to reinvest dividends in their calculations, which understates actual growth.

Avoiding these errors leads to more realistic expectations.

When Manual Calculation Is Useful

Manual MP2 calculation is best for understanding concepts and validating results. For detailed planning, calculators are more practical.

Manual computation is especially useful when you want to:

-

Learn how MP2 dividends work

-

Check whether a calculator result makes sense

-

Explain MP2 to others clearly

For quick and accurate estimates, calculators remain the preferred option.

Final Thoughts

Learning how to calculate Pag-IBIG MP2 manually helps you understand the mechanics behind your savings. While manual calculations require effort and assumptions, they provide valuable insight into how dividends and reinvestment work.

Once you are comfortable with the process, you can confidently use MP2 calculators to plan your contributions and track progress. Understanding both manual and automated methods puts you in control of your MP2 savings decisions.