If you are exploring long-term savings options in the Philippines, you have likely encountered the term Pag-IBIG MP2. Many Filipinos consider MP2 as one of the most practical and accessible ways to grow their money through a government-backed savings program.

This guide explains what Pag-IBIG MP2 is, how it works, who can invest, and why it has become a popular choice for disciplined savers.

This page is written to give you a clear and complete understanding of MP2 before you use any calculator or commit your money. It focuses on fundamentals, rules, and realistic expectations rather than projections alone.

What Is Pag-IBIG MP2?

Pag-IBIG MP2, formally known as the Modified Pag-IBIG II Savings Program, is a voluntary savings program offered by Pag-IBIG Fund. It is designed to help members earn higher dividends compared to the regular Pag-IBIG savings, while still enjoying the security of a government-managed fund.

Unlike mandatory Pag-IBIG contributions, MP2 participation is optional. Members have full control over how much they invest and how often they contribute. The program has a fixed maturity period of five years, after which savings and dividends can be withdrawn or reinvested.

How Pag-IBIG MP2 Works

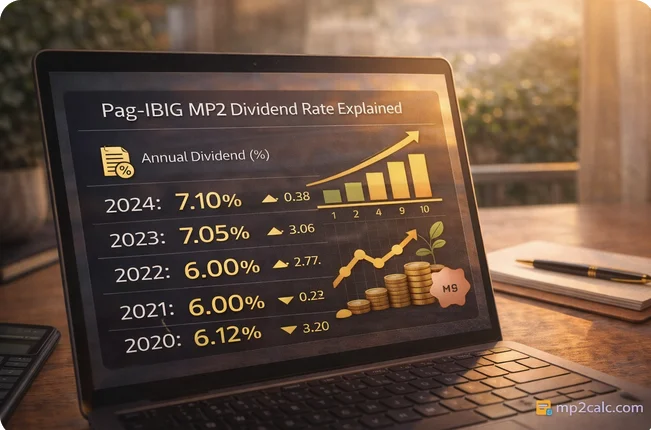

MP2 operates on a dividend-based model. Contributions are pooled by Pag-IBIG Fund and invested in housing finance, government securities, and other approved instruments. At the end of each year, Pag-IBIG declares an MP2 dividend rate based on fund performance.

Once dividends are declared, they are credited to each member’s MP2 account. These dividends are usually reinvested automatically, allowing them to earn additional dividends in subsequent years. This compounding effect is one of the main reasons MP2 is attractive for long-term savers.

Dividends are not fixed and may vary from year to year. While MP2 has historically offered competitive returns, it is important to understand that dividend rates are not guaranteed.

Who Can Invest in Pag-IBIG MP2

Pag-IBIG MP2 is open to a wide range of members. You may invest in MP2 if you are:

-

An active Pag-IBIG member

-

A former Pag-IBIG member with prior contributions

-

A retiree who previously contributed to Pag-IBIG

-

An Overseas Filipino Worker (OFW) with Pag-IBIG membership

This flexibility makes MP2 accessible to both employed and self-employed individuals, as well as Filipinos working abroad.

MP2 Contribution Rules and Flexibility

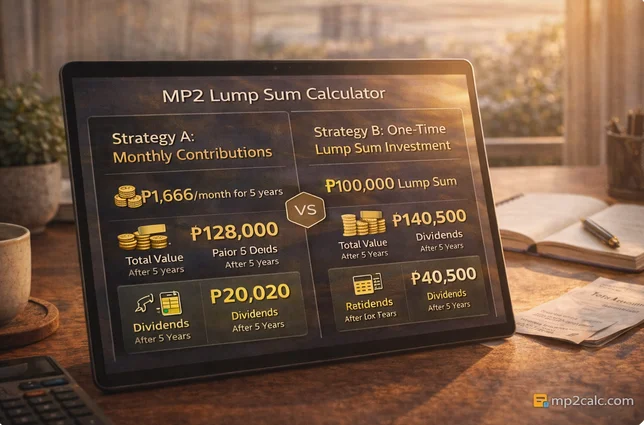

One of the strengths of the MP2 program is its flexibility. The minimum contribution is ₱500 per remittance, and there is no maximum limit. Members may contribute as often or as irregularly as they wish.

You may choose to invest through:

-

Monthly contributions

-

Annual contributions

-

One-time or lump-sum deposits

This flexibility allows MP2 to adapt to different income patterns and financial situations. To see how different strategies affect your savings, you may use the Pag-IBIG MP2 Calculator.

MP2 Maturity Period Explained

The MP2 program has a fixed maturity period of five years. During this time, funds are generally locked in and earn dividends annually. At the end of the five-year term, members may withdraw their total contributions and dividends.

Members who prefer to continue saving may choose to open a new MP2 account and reinvest their funds. To understand how much you may receive at the end of the term, you can use the MP2 Maturity Calculator.

Are MP2 Dividends Tax-Free?

Yes. One of the major advantages of MP2 is that all dividends are tax-free. This means the amount credited to your account is the amount you receive, without deductions.

Because of this tax advantage, MP2 often compares favorably with other low-risk investment options such as bank time deposits.

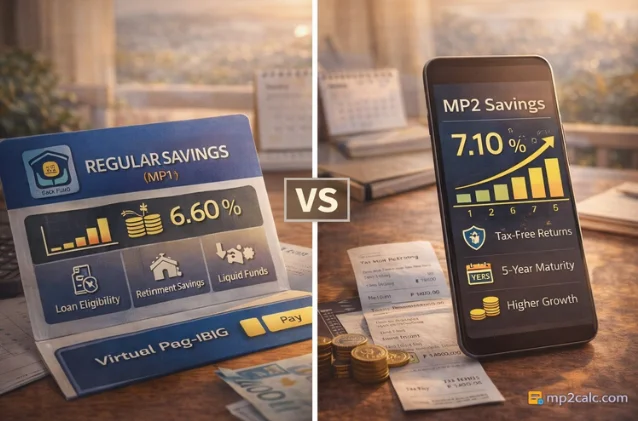

MP2 vs Regular Pag-IBIG Savings

While both programs are managed by Pag-IBIG Fund, MP2 differs significantly from the regular Pag-IBIG savings program.

Regular Pag-IBIG savings are mandatory and primarily serve as a requirement for housing and loan eligibility. MP2, on the other hand, is voluntary and focused on savings growth.

MP2 typically offers higher dividend rates but comes with a fixed maturity period. Understanding these differences helps you decide whether MP2 fits your financial goals.

Risks and Considerations You Should Know

Although MP2 is government-managed, it is still important to understand potential risks. Dividend rates depend on fund performance and may change yearly. MP2 is also less liquid than regular savings accounts due to its five-year lock-in period.

These factors mean MP2 is best suited for money you do not need for short-term expenses.

Why Many Filipinos Choose MP2

Filipinos choose MP2 because it combines security, flexibility, and competitive returns. It is easy to start, requires a relatively low minimum contribution, and does not require advanced financial knowledge.

MP2 is often used as a supplement to other savings or investment plans rather than a replacement for emergency funds.

Frequently Asked Questions About Pag-IBIG MP2

1. Is MP2 a good investment?

MP2 is considered a low-risk savings option with tax-free dividends, making it attractive for conservative investors.

2. Can I have more than one MP2 account?

Yes. Members may open multiple MP2 accounts if they wish.

3. What happens if I stop contributing?

Your existing MP2 savings will continue to earn dividends based on the declared rate.

Final Thoughts

Understanding what Pag-IBIG MP2 is and how it works is the first step toward using it effectively. MP2 is not a get-rich-quick scheme, but it is a practical and disciplined way to grow savings over time.

Once you are comfortable with the basics, you can explore projections using the Pag-IBIG MP2 Calculator or test specific strategies using the dedicated MP2 calculators available on this site.